The global crisis of recent years has led the media to focus on digital, to devise new business models to face it, to form in new narrative forms and to explore new ways of disseminating content. Both the events of 2022 and the trends and forecasts of 2023 point in the same direction, the changes will not stop. We are even at the door of artificial intelligence, domesticated, turning into a new era. There will not be a single means of subsistence and success, but in an increasingly complex playing field, the activity of identifying keys and finding answers will be a joint exercise of communication highways in Basque.

Reviewing international communication trends in 2023 has focused on three reports: Digital News Report 2022 (Newman et al., 2022); The kaleidoscope: tracking young people’s relationships with news (Craft & RISJ, 2022); and Journalism, Media, and Technology Trends and Predictions 2023 (Newman, 2023). The three have been published by the Reuters Institute, which aims to analyze the future of journalism. These are important reports to outline the time in which we live, hence this article, which is a compilation of significant international events, has focused on them. We will present 11 keys to understanding the field of media play, work on the relationship of young people with news and describe five axes for the future of journalism.

11 KEYS TO UNDERSTANDING THE MEDIA PLAYING FIELD

The eleventh edition of the Digital News Report 2022 has again clarified the major challenges facing industry from data from six continents and 46 markets. Authors of the Reuters Institute study (Newman et al., 2022).

While the 2021 study showed positive signals for the information sector – increased use and confidence – these indications have not been maintained in the 2022 data collection: interest in news and audience data has been reduced in many countries; and the confidence indicator has not been increased. The fatigue of receiving and processing information is spreading, and more and more people decide to avoid news (Tubia, 2022).

Disconnecting from news

The challenge of the basic era that we live for any media is to connect online with a user with more online content than ever before and convince that attention to news is worth it.

The report contains data of a decade in which there is a progressive decline in the reach of traditional media in all countries: press, radio and television. At the same time, the online reach remains stable, or in the best cases increases slightly, but in no case covers the vacuum. Digital media and social media offer a much broader range of information, but this offer can often be excessive and confusing.

Less interest in news

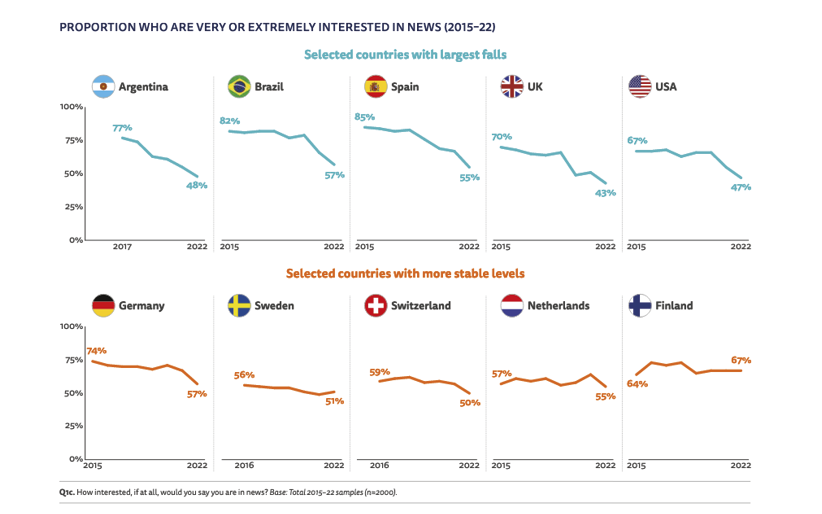

The percentage of people who claim to be ‘very’ or ‘terribly’ interested in news has been significantly reduced over time: Data from 2022 show that interest in news is lower in most study countries. Sometimes, in Argentina, Brazil, Spain or the United Kingdom, these falls have been accumulating for years. Instead, in the United States, the model is something different. During Trump’s years, great interest remained and since Joe became president of Bide he has gone down. In other countries such as Germany, Sweden, Switzerland, the Netherlands or Finland the level of interest is more stable.

Considering all international developments, less than half of the respondents (47%) claim to be "very" or "very" interested in news – 67% in 2015.

The phenomenon has two related problems: on the one hand, the widespread drop in interest and consumption for news that have been rejected by a minority of users active in the network, may not be relevant to their lives; and on the other, the general decrease in interest and consumption for news that affect a much larger group and that may be associated with structural changes in the way news is distributed, such as the transition to digital or the change in the character of the information cycle.

Avoiding certain news items

More and more people are dosing or limiting exposure to news or at least to a certain type. This behavior, known as “selective news rejection”, can help explain why overall consumption levels have not increased.

The rate of occasional or frequent news avoidance has doubled since 2017 in some countries, such as Brazil or the United Kingdom, and has increased in other markets.

A large number of users, especially the younger ones, consume the news in a fragmented way – via batteries shared on social networks or messaging applications. Around the Coronavirus or in connection with the war in Ukraine, many media outlets have chosen to publish on their websites and social networks usage formats (called explainers) and, in the light of the data, the media should delve into this path.

Low trust

This year, the numbers show a lower overall level of confidence in 21 of the 46 countries studied – only seven show an upward trend – and an average level of confidence (42%) slightly lower than in 2021.

In addition, in countries with greater confidence, such as Finland, there is a greater interest in and a lower tendency to avoid news. On the contrary, in untrustworthy places like the United States. France, the United Kingdom or Slovakia have rates of selective rejection, disconnection and declining interest.

However, it is appropriate to contextualize the changes around the level of confidence shown in this year’s report, although in most cases the indicator remains above the pre-pandemic level.

In many countries in Northern and Western Europe, as well as in Canada and Australia, the degree of trust in news is driven by various public media with a high degree of independence. These media are often the first opportunity for citizens seeking reliable information on important issues. They are often organizations whose brand perception is very different from that of the public media in Southern and Eastern Europe, and they do not have a tendentious editorial line. However, independent public media are increasingly being pressured by attacks on funding, doubts about its impartiality and difficulties in accessing digital media and social media in some countries.

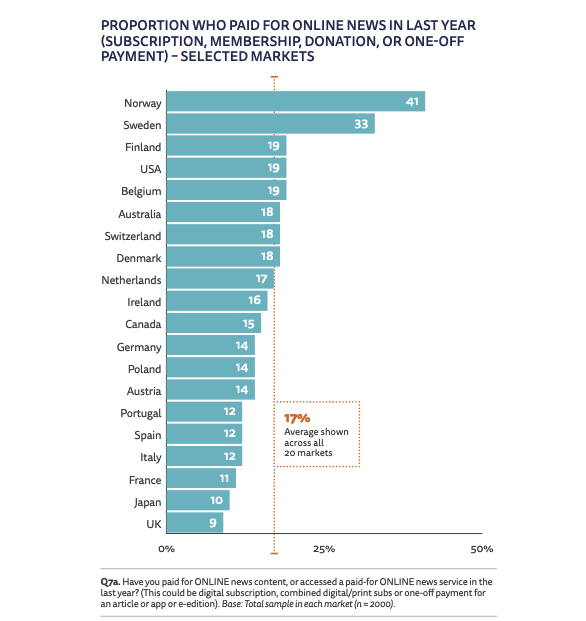

Payment for news, subscriptions and user registration struggle

In recent years, the media has intensified efforts to make users pay for network content through subscriptions, partners or donations, thus reducing revenue dependence.

This year’s report shows remarkable growth in a few rich countries, but in others there are signs that can stabilise growth. In a group of 20 countries with a tendency to pay fairly generalized, 17% of the population has paid for online news, the same data as in 2021.

In all countries, the heads make up the vast majority of the payers, with an average age of 47 years. A fundamental problem for industry is to persuade young people to pay, for example, 28% of Spanish and French subscribers are under 30.

Most subscribers pay for a single post, but in the U.S. and Australia about half (56 per cent and 51 per cent respectively) currently pay two or more media, often combined with national and local newspapers.

Do not upgrade but register to continue navigation

Beyond concerns about the evolution of subscription data, the media industry faces the challenge of maintaining advertising revenue by the short-term disappearance of third-party cookies. To counteract this, companies try to collect first-hand data, get relevant information for companies and find ways to increase their rates. Consequently, in the context of the media, an electronic address is required to access certain complementary content or functions.

But how does the public meet these demands? Users are reluctant to assign their email or other personal data, especially if the same content is available elsewhere. Furthermore, most media do not have a clear proposal of values to convince people to register.

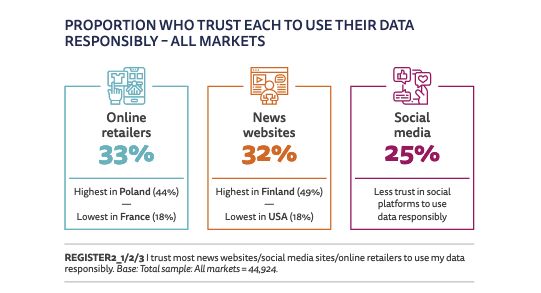

According to general data from the Digital News Report 2022, only a third of users (32%) consider that the media makes responsible use of personal data, so the media is above social networks (25%), but at a level similar to that of online stores (33%).

In any case, trust in the media varies considerably across the country: for example, 49% of Finns are willing to give their data to the media, down to 18% among Americans. There is therefore a clear link between general confidence and the willingness to provide data to the media. Confidence-building will be crucial not only for the media that wish to promote subscription models, but also for anyone who intends to connect with audiences in the future.

Access to news

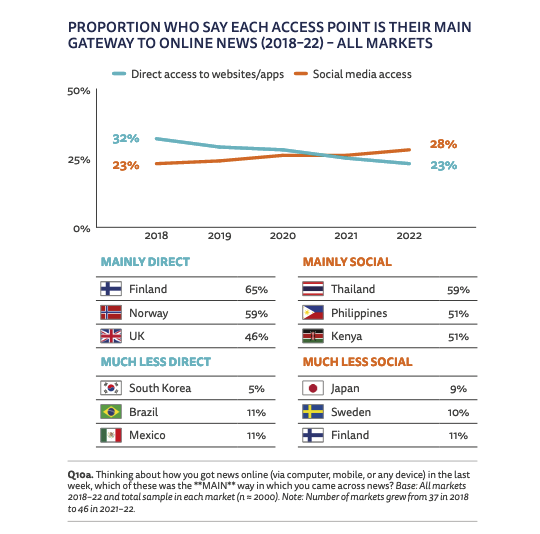

What channels do people choose in the mornings to access news on their mobile? Since 2019 social networks have surpassed pages and applications.

This year the sector has reached a turning point, as the priority for social networks (28%) has exceeded direct access to the media (23%).

In any case, above market averages there are large differences between countries. Thus, perhaps, in the light of the data, it could be thought that promoting subscriptions to news consumption in countries with higher direct access rates.

To a large extent, the dominance of social networks in the face of direct access is a change produced by the habits of a new generation, social natives, which is currently maturing. This young generation, under the age of 24, who has grown up with social networks, is not only different from the previous ones, but is also more different from the previous ones and shows a much weaker relationship with media brands that had previously been common.

Social networks as a means of media consumption

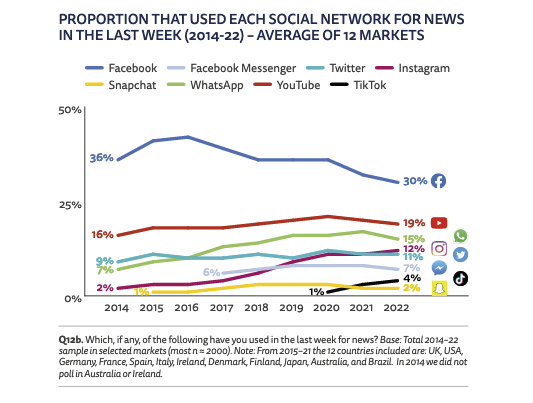

Since 2014, the Institute Reuters has monitored the use of social networks in 12 countries, observing their use in the following two cases: ‘for any purpose’ and ‘for news’.

Global use of Facebook for any target (60%) drops five points at the 2017 summit, while the only ones that have grown in the last year are Instagram (40%), Tik Tok (16%) and Telegram (11%). Also in this case, the behavior of younger people is the engine of change and not that of a group of older adults with more entrenched habits.

As regards news consumption, Facebook remains the most important benchmark among social networks – although it has dropped 12 points since 2016. Twitter has maintained its same number of users-server in the last decade, without major oscillations, and continues to have a strong influence between politicians and journalists; however, by the end of 2022, the loss of users of the network for $44 billion that Elon Muskiz will suffer in the next report — according to the market research agency Insider Intelligence, will lose 32 million blue users in the next two years, Intelligence). The Instagram network, owned by Meta, is becoming more and more used for news, and Tik Tok has come to overcome – although it still has a low base – Snapchat.

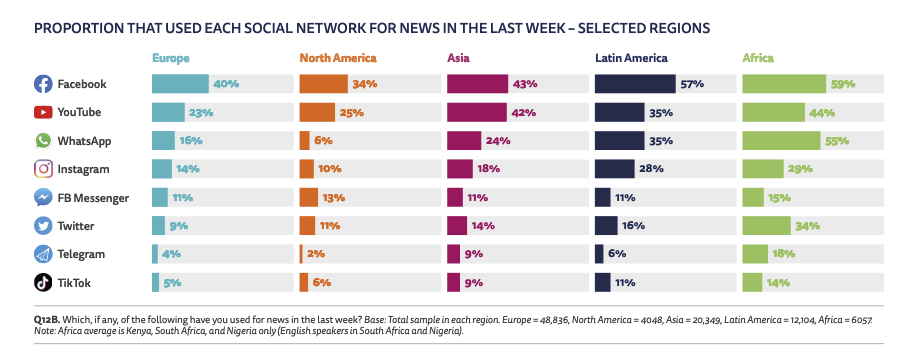

Outside Western countries, especially in Latin America and Africa, the share of social media use for news is much higher.

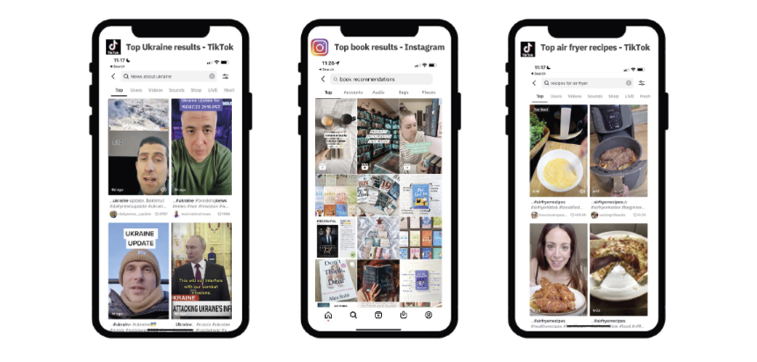

The information ecosystem is visited by Tik Tok

Significant and rapidly growing global use of the Tik Tok network, mainly in Africa, Asia, Latin America and Eastern Europe, among those under 25 years of age.

The Ukrainian war has expanded the role of using the platform for information purposes. Although some think that the network where entertainment content predominates is not the most effective place for news, the BBC News, for example, created channels in Russian and English to combat the misinformation of war.

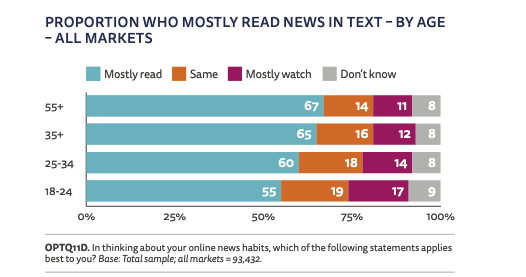

Video information? No, more in the text

Since the creation of the Internet, the consumption of web pages (and applications) that offer news has been based on reading articles, on the primacy of the text, but this has started to change with the growing supply of video formats offered by social networks.

The authors of the Reuters Institute study last asked respondents in 2019 what they preferred, read the news or watch it on video. In 2022, they"ve been interrogated again, and the picture hasn"t changed much. Today text is preferred in all age groups.

In general, respondents say they prefer to read because it is faster (50%) or because it gives them more control (34%). Conversely, those who prefer to watch the news on the Internet via video consider the audiovisual media to be a simpler (42%) and attractive (41%) mode, whereas a quarter opt for video because they use social networks and appear on them (24%).

New podcast use

Following the pandemic cut, podcast growth has regained in more than half of the markets surveyed in 2022. In these countries, the rate of users who have confirmed listening to one or more podcasts in the last month has been 34% (three points higher than the previous occasion) and 12% the audience of a news podcast. Ireland’s long-standing audio tradition leads the podcast usage list (46%) alongside Sweden, Spotify’s native region (44%).

Spotify, Amazon and Google invest in podcasts seeking to take advantage of the growing demand for this format, which tries to break Apple’s old domain by fichating talented stars.

Big technology platforms invest in content and work to attract a broader audience through programming, but this movement worries the media like monetization, distribution or access to data. In this scenario, the New York Times will launch its audio application this year to create direct traffic.

HOW DO YOUNG PEOPLE RELATE TO NEWS?

It is clear that young audiences show different behaviors regarding news. At the request of the Reuters institute, and completed the study by the Craft agency, the issue has been discussed in depth in a report released in autumn 2022: The kaleidoscope: tracking young people’s relationships with news (Craft & RISJ, 2022). In it, besides analyzing the phenomenon, suggestions are offered to adapt the news to these young audiences.

The first objective of the report: the news for young people is not just digital, they are social. They grew up with the social web and participant, which has completely conditioned the current consumption of news, which is the "news" and the confidence in who they trust.

The second main line is that the consumption behavior of young people is not unique, but they show a kaleidoscopic behavior and attitude —which could not otherwise be in a fragmented media environment, in full format and brand growth and taking into account the natural diversity of the group—.

The main findings of the report are presented below.

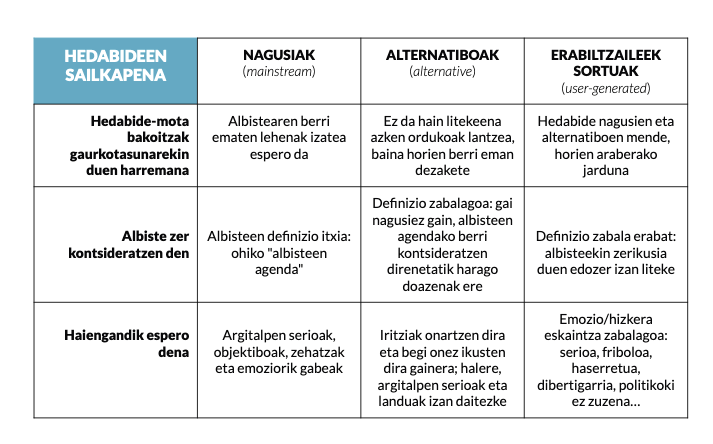

News can be “narrow” or “broad”

Young people distinguish between ‘the news’ and ‘news’, a traditional agenda that is closely linked to politics and today, and a broad agenda with topics such as sports, entertainment, famous expressions, culture and science. The first relates to the main traditional media, with the brands in which it is expected to act impartially and objectively, while the second is a broader category and a more varied range of shades in the alternative media classified here. In addition, this dichotomy breaks with the news generated by users, and in this more open definition drawer you can locate virtually everything that is found on the network.

There are those who consciously dodge the “close and serious” news

In general, instead of avoiding the news, there is talk of “certain news to avoid”, often as a strategy to care for mental health. Young people prefer news from alternative media to mainstream media, and this bias has consequences for major brands, as their serious position does not help them connect with this potential audience.

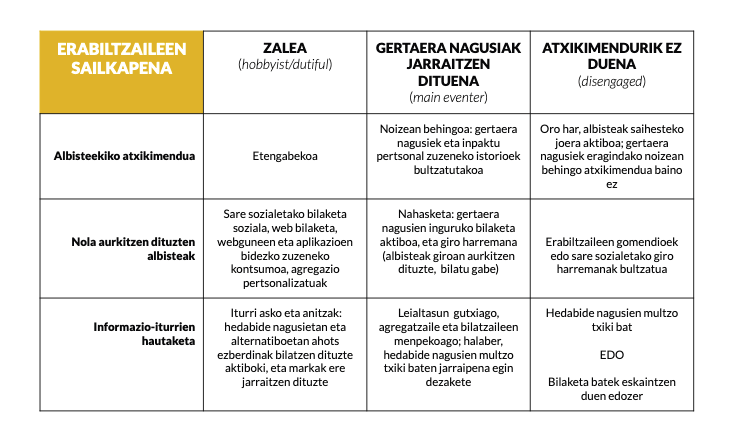

Factors influencing youth consumption preferences

Behind one behavior or another, personal and contextual factors come into play. The increase in opportunities spread by the social web that focuses on the consumption of mobiles has made the consumption preference of each young person different and practically unique. To understand what is happening, the types of users have been divided into three categories: amateurs, those who follow the main events and those who have no attachment. The former consume news to shape the civic obligation to enjoy and know what is happening; the latter have the practical need to follow the facts that influence their daily lives—for them it is not a joy or an obligation—and the third parties only follow the most important events that must be known.

They"re very skeptical about most of the information

Sometimes they go beyond being skeptical and often question the agenda of major news providers. As they have grown up in the digital age and educated older generations to be critical of the information they consume, they judge the major brands based on their impartiality.

The format you prefer is a matter of taste

When it comes to exploring the format preferred by the young people, the answers are not very dense, but the predominance of choice according to each is a matter of taste. They like different formats and supports, and there"s a track that you can follow, that attracts the information that"s ready for them. The text will continue to take its place, whether it be videos, audio or images, and many times they will want to concentrate everything on one content.

Brands in the main media cannot constantly satisfy all young people, but there seems to be a chance of being chosen more often, they can do something: diversify offers, broaden the agenda and attenuate the tone. In short, rather than attracting the less engaged group, try to walk towards them. To do so, they should take into account who produces the news addressed to young audiences and their suitability to the codes and standards of the platforms where such content is disseminated.

FIVE AXES FOR THE FUTURE OF JOURNALISM

The report Journalism, Media, and Technology Trends and Predictions 2023 (Newman, 2023), published annually by the Reuters Institute researcher Nic Newman, has beentaken as a basis for clarifying trends this year. The core of the study is the surveys of 303 executives from 53 international countries, a reflection of a strategic sample of leaders of the media industry, which is not representative, but includes the speculation of the author, but rather a reading suggestive to take into account in our time.

Inflation and uncertainty (threat)

The war in Ukraine has brought the energy crisis and inflation out of hand, but not only that, it has also reminded us of the need for local information and expert analyses in times of uncertainty.

As far as advertising is concerned, advertisers are shrinking, citizens are reducing their household expenses and the media are facing rising costs. By the end of 2022, this perfect storm caused redundancies, cost freezes and other restrictive measures.

When the media representatives were asked about confidence in their business prospects by 2023, the group that showed certainty did not reach half (44%), those that showed uncertainty (37%) and those that showed little confidence (19%) predominated.

The most affected have been those who still have a strong dependence on paper publications, in some cases doubling the price of paper. In any case, digital creation companies, affected by the decrease in traffic from large platforms such as Facebook and Twitter, especially those that depend on the deployment of social networks, are also not released.

Any publication that is highly dependent on print copies or advertising revenue will this year have serious problems. In this regard, and given that local newspapers are particularly vulnerable, the government is likely to be able to intervene more to support the sector in some countries.

Radio and television channels are also experiencing increasing problems due to the rapid decline in audiences across all age groups. Netflix’s decision to accept advertising will increase pressure, while public chains will suffer funding restrictions.

|

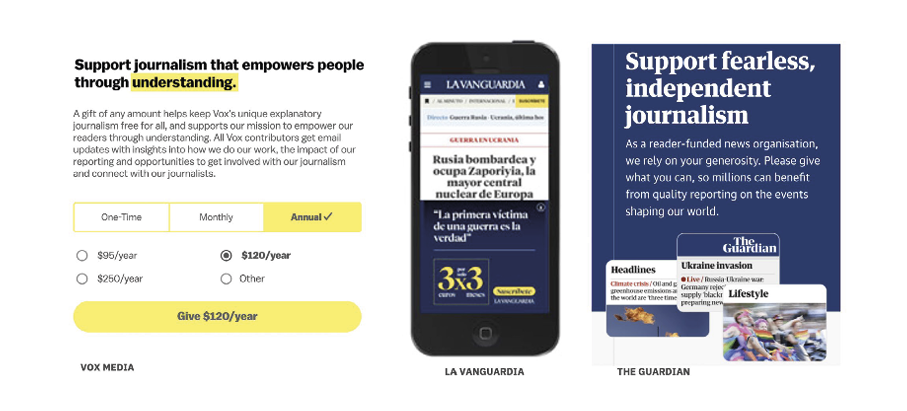

Expectation of digital subscriptions

Important media with printed publications are placing their hope in digital subscriptions, partners and donations. For example, 70,000 subscribers have been added to The Times over the past year, and the New York Times is increasing their subscriptions -- 10 percent last year -- in a career of 15 million set up by 2027. However, there are voices that say whether subscriptions have hit the ceiling. This year’s focus will be on keeping existing subscribers rather than adding new ones.

For those wishing to maintain the new subscribers obtained, the two movements will be fundamental: lower prices and special offers, on the one hand, and to underline their role and values.

Another movement that has spread is to try to retain subscribers by offering them complementary products or brands. The New York Times, for example, offers a basic information package, kitchen with its app, games and Wirecutter, a service that offers product reviews and referrals, or another modality combining information and broad sports coverage such as The Athletic, which are already the main focus of your subscription increase.

Multiple media outlets will try to copy the play:

- Work in developing premium products such as play, cooking, books, podcasts or newsletters.

- Acquisition of other entities, success niches and based on subscriptions.

- Transform existing brands into ancillary products.

Le Figaro, for example, is adapting the New York Times strategy and in Norway have launched a very interesting collaborative approach: The main Norwegian newspaper from Aftenposta offers a package together with other brands from the Schibsted group (Norwegian International Media Group) that can be consumed by a single subscription on the PodMe application (Norway, Sweden and Finland’s exclusive podcast advertising platform).

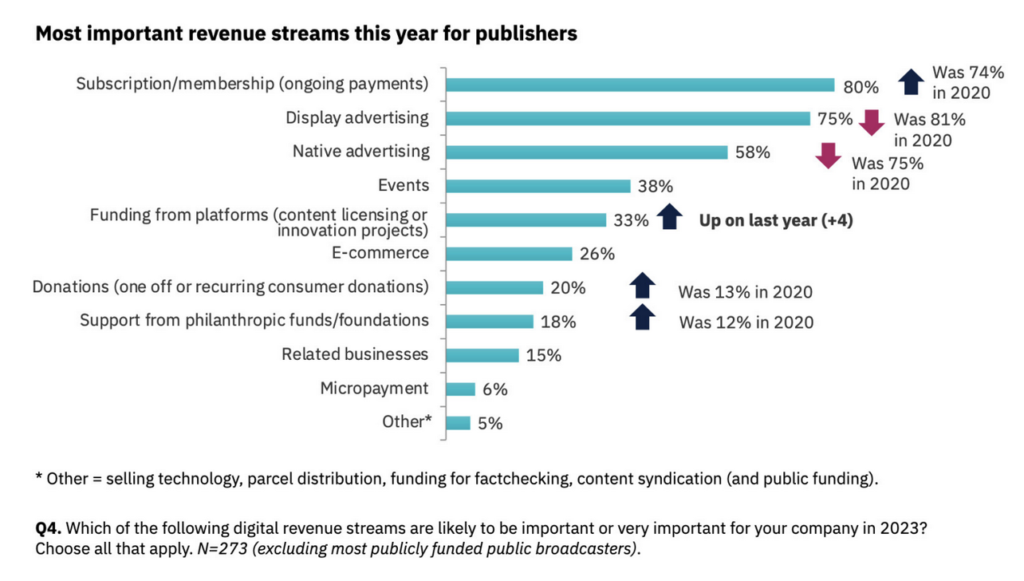

Subscriptions remain the top priority in the survey (80%), followed by online advertising (75%). However, most media advocate the importance of having different sources of income, prioritising diversification.

According to the report, the financing combinations of some major media are:

- The Guardian: subscriptions + digital advertising + platform revenue, collaborating entities and events.

- The Financial Times: subscriptions + native advertising and display + a consultation with other media companies - the FT Weekend Festival is expanding the event business.

Beyond paid content, the most recent source of revenue has been funding through technology platforms. In the European Union, Google currently pays for more than 300 media, as is the case in other parts of the world such as Australia or Canada. Facebook has also paid 20 million dollars to include the content of some major media in its news section.

|

The maximum of the Internet and the challenge of those who avoid the news

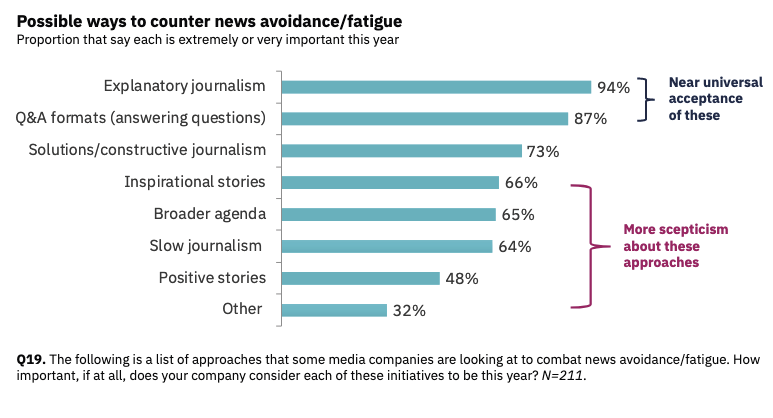

After years of sustained growth, the time devoted to the network begins to descend according to the company investigating the GWI audience: The total time spent on the Internet has been reduced by 13% following records of use made in containment during the pandemic, which may indicate that we have reached the peak (GWI, 2022).To avoid selective news avoidance or certain fatigue, most respondents have opted for two mandatory working formats in 2023: journalism (94%) and the question-answer format (87%).Euskal Hedabideen Behategiko koordinatzailea - NOR Ikerketa Taldea, UPV/EHU

|

Start suffering the platforms

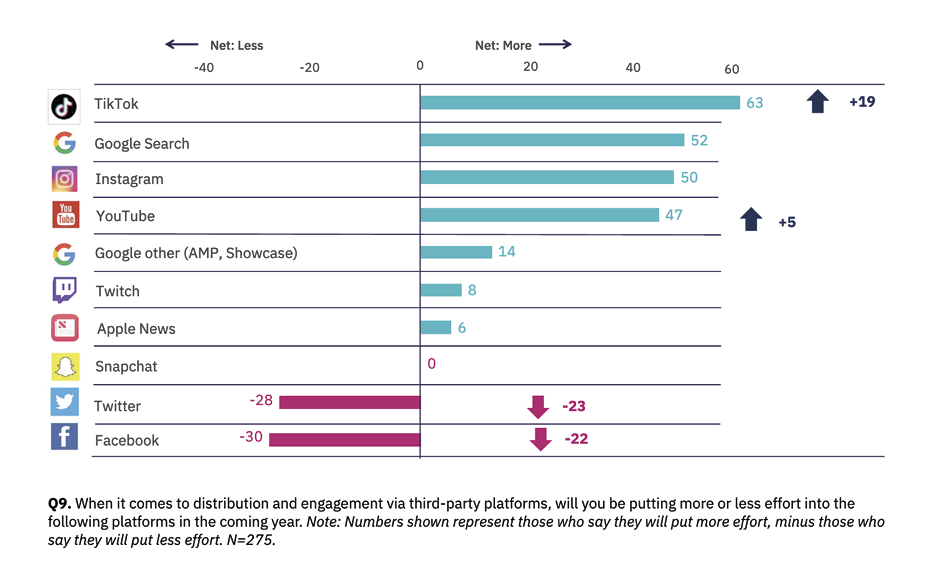

In the last year, Twitter dismissed three-quarters of its employees and departed from major advertisers. Meta"s actions have dropped by about two-thirds and the concern of some workers has been put on the table as a complaint: Mark Zuckerberg’s obsession with the metaverse endangers the company’s survival. Meanwhile, among younger users, especially among younger users, it is perceived that first generation social networks lose attractiveness, highlighting applications such as Tik Tok “more fun”. Few could imagine a seismic sequence of these characteristics a year ago.The spectacular rise of Tik Toke, owned by the Chinese giant ByteDance, already has a billion users a day. This breakthrough is not only worrying existentially for Facebook; Google has also begun to notice that some of the traffic based on their searches is disappearing, and Amazon is following the process on alert for the potential of the Tik Tok network as a platform for buying and paying.On the other hand, Elon Muskiz"s behavior before and after buying Twitter for $44 billion has removed journalists and some citizens from the social network. Concern grew at the end of 2022, including the dismissal of workers seeking to ensure the integrity of the platform, the abandonment of the accounts of critical journalists and claims about the blue mark for certified sources. The bird lost many users last year, and other networks populated by users who left, such as Mastodon, which seems not to be replaceable (Nicholas,2023).In this context, the survey conducted by the Institute Reuters with media representatives highlights changes in media approaches to social networks: They say they will offer fewer resources to Facebook and Twitter, and more to Tik Toki, to the Google search engine, to Instagram and to the YouTube network. These data clearly indicate that video platforms such as YouTube and Tik Tok will be given priority in 2023, as will the Instagram network. Media representatives believe that they are a good means of attracting young audiences. Another thing is that in these platforms the internal consumption of the platform predominates, with the consequent decrease in traffic in the media portals, and in the same sense, artificial intelligence will be a great challenge in the media network strategies based on clicks or visits (Benton,2023).

These data clearly indicate that video platforms such as YouTube and Tik Tok will be given priority in 2023, as will the Instagram network. Media representatives believe that they are a good means of attracting young audiences. Another thing is that in these platforms the internal consumption of the platform predominates, with the consequent decrease in traffic in the media portals, and in the same sense, artificial intelligence will be a great challenge in the media network strategies based on clicks or visits (Benton,2023).

|

Advances in artificial intelligence and journalistic applications

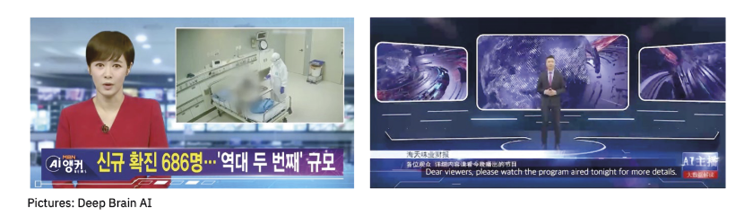

Artificial intelligence chatotas (AA) have been the subject of mockery and truffle, but the arrival of OpenAI ChatGPT has transformed the debate. Although the model on which it is based exists for a long time, ChatGPT has given it the form of an accessible prototype, and the clear idea of what can be done when deploying AA has been made public by the end of 2022: it is able to tell jokes, to devise arguments for a film or book, writes computer codes or can summarize the challenges of local journalism if it so requests.Many voices speak of transformation: Some believe that ChatGPT is one of the greatest technological developments since the invention of the Internet and that it is part of a wider trend called ‘creative AA’, as computers can produce not only words but images, videos and even virtual worlds.Artificial intelligence allows us to streamline processes and use some existing elements to build something new. This change raises some existential concerns for the journalist, but it also opens up a range of possibilities. The consequences for journalism are not yet clear, but while some journalists are starting to use tools like MidJourney and DALL-E to create illustrations for publications. There"s some more ambitious media, like Semafor: Under the name of WITNESS he created several videos of Ukraine"s image-free testimonials dressed in AA animations (Lukyanova, 2022).Conversely, similar deep learning models and counterfeiting of reality can be used as a fake video calling for President Volodymyr Zelensky to leave the guns (Wakefield, 2022).It is possible that in the coming years there will be an explosion of automated and semi-automated content, both for better and for worse, in which it will be easier than ever to create attractive and credible multimedia content, but it will be harder to distinguish between real and false than ever.

|

REFERENCES

BBC. (2022). Plan to deliver to digital-first BBC. <https://www.bbc.co.uk/mediacentre/2022/bbc.com/mediacentre/2022/plan-to-deliver-a-digital-first-bbc/>

Benton,J. (2023). GooglenowwantstoansweryourquestionswithoutlinksandwithAI.Wheredoesthatleavepublishers?NiemanLab.<https://www.niemanlab.org/2023/02/google -now-wants-to-answer-your-quest-without-links -and-con-ai-where-does-that-leave publishers/>

Cavender,E. (2022). ForGenZ,Tik Tokismorethanentertainment.It’sasearchengine.Masspeak.<https://mashable.com/article/gen-z-tiktok-search-engine-google>

Craft&RISJ. (2022). TheKaleidoscope:YoungPeople’sRelationshipsWithNews.<https://reutersejerc%politics .ox.ac.uk/sites/default/files/2022-09/Craft%20%26%20RISJ%20-%20The%20Kaleidoscope%20-%20Young%20People%27s%20Relationships%20News%20.pdf

GWI. (2022). Connectingthedots:Theconsumertrendstoknowfor2022.<https://www.gwi.com/hubfs/CTD%202022%20 -%20videos%20and%20pdfs/PDFs/Connecting%20the%20dots%202022.pdf>

InsiderIntelligence. (2022). TwitterWillLoseMorethan32MillionUsersWorldwideby2024AmidTurmoileMarketerNewsroom.<https://www.insiderintellig{\{\}com/newsroom/index.php/se -will-lose-more -than-32-million-users-worldwide-by-2024-amid-turmoil/>

Lukyanova,T. (2022). LifeduringtheRussianoffensive,illustratedbyartandAI|Semafor.<https://www.semafor.com/article/10/20/2022/ukraine-reconstructed-memory-video> <https://www.semafor.com/article/10/20/2022/tango-reviewer/video>

Newman,N. (2023). Journalism,Media,andTechnologyTrendsandPredictions2023.ReutersInstitutefortheStudyofJournalism.<https://reutersbancos .politics .ox.ac.uk/sites/default/files/2023-01/Journalism_media_and__trends_and_predict_2023.pdf>

Newman,N.,Fletcher,R.,Robertson,C.T,Eddy,K.,&Nielsen,R.C. (2022). ReutersInstituteDigitalNewsReport2022(p. 164). ReutersInstitutefortheStudyofJournalism.<https://reutersbancos .politics .ox.ac.uk/sites/default/files/2022-06/Digital_News Report_2022.pdf>

Nicholas,J. (2023). ElonMuskizdrovemorethanamillionpeopletoMastodon–butmanyaren’tstickingaround.TheGuardian.<https://www.theguardian.com/news/datablog/2023/jan/08/elon-musk-drove-more -than-a-million-people-to-mastodon-but-many-arent-sticking -around>

Tubia,I. (2022). Running away from theusualnews.New.<https://www.berria .eus/paper/1906/030/001/2022-09-28/habitual-informativos -ihesi .htm>

Wakefield,J. (2022). Deepfakepresidentsusedin Russia-Ukrainewar—BBCNews.<https://www.bbc.com/news/-60780142>